When debt becomes overwhelming, many people look for fast solutions. Credit counseling agencies often market themselves as trusted organizations that can help consumers regain control of their finances. On the surface, that sounds like a smart move.

But credit counseling is not always the financial lifeline it claims to be.

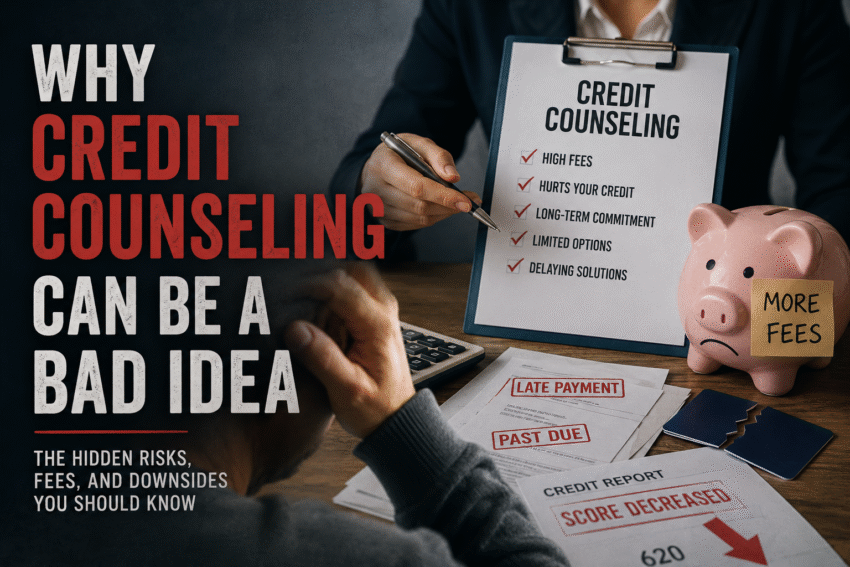

In reality, some consumers end up paying unnecessary fees, damaging their credit, or delaying better solutions because they didn’t fully understand how credit counseling works. Before signing up, it’s important to know the potential drawbacks.

What Is Credit Counseling?

Credit counseling typically involves working with an agency that reviews your finances and recommends a debt repayment strategy. Many agencies push consumers into Debt Management Plans (DMPs), where the agency negotiates with creditors and collects monthly payments from the consumer.

While this may help certain people organize debt repayment, there are several reasons why critics argue credit counseling can create more problems than it solves.

1. It Can Hurt Your Credit

One of the biggest misconceptions is that credit counseling has no impact on your credit score.

In many cases, enrolling in a debt management plan requires closing credit card accounts. Closing accounts can reduce your available credit and shorten your credit history, both of which may lower your score.

Even if your score doesn’t drop immediately, lenders may view participation in a debt management plan as a warning sign that you are struggling financially.

For someone hoping to buy a home, refinance a loan, or qualify for new credit, this can become a major obstacle.

2. Fees Add Up Quickly

Many people assume nonprofit credit counseling means “free.”

That is not always true.

Some agencies charge:

- Setup fees

- Monthly maintenance fees

- Educational course fees

- Late payment penalties

Over time, these costs can add hundreds or even thousands of dollars to your overall debt burden.

In some situations, consumers discover they could have negotiated directly with creditors themselves for little or no cost.

3. Not All Agencies Are Trustworthy

The credit counseling industry has a mixed reputation.

While there are legitimate organizations, others operate more like sales companies focused on enrolling as many clients as possible. Some agencies use aggressive marketing tactics that prey on people who are stressed and financially vulnerable.

Consumers may be pressured into repayment plans without fully understanding:

- The long-term consequences

- The total fees involved

- Alternative options available

Some agencies also blur the line between true counseling and debt settlement services, which carry additional risks.

4. Debt Management Plans Are Extremely Rigid

Debt management plans often require strict monthly payments over three to five years.

Miss a payment, and the arrangement with creditors may collapse.

For families dealing with job loss, medical emergencies, or fluctuating income, these plans can become difficult to maintain. Once a plan fails, consumers may end up back where they started — except with more fees and wasted time.

5. It May Delay Better Solutions

Credit counseling is often presented as the “responsible” alternative to bankruptcy. But in some cases, bankruptcy may actually be the faster and more effective path to financial recovery.

Consumers who spend years struggling through unrealistic repayment plans sometimes end up filing bankruptcy anyway — after draining savings and retirement accounts trying to keep up.

That delay can make financial recovery even harder.

6. You Can Often Do It Yourself

Many of the services provided by credit counseling agencies can be done independently:

- Creating a budget

- Negotiating lower interest rates

- Requesting hardship programs

- Setting up payment arrangements

Creditors are frequently willing to work directly with consumers, especially if payments are already becoming difficult.

By handling negotiations yourself, you avoid third-party fees and maintain more control over your finances.

When Credit Counseling Might Help

To be fair, credit counseling is not always bad.

A reputable nonprofit agency may help consumers who:

- Need budgeting guidance

- Want financial education

- Have manageable debt and stable income

- Need structure and accountability

The key is understanding that credit counseling is not a miracle solution — and it is not risk-free.

Final Thoughts

Debt problems create stress, urgency, and fear. That makes consumers especially vulnerable to promises of quick financial relief.

Before enrolling in any credit counseling program, take time to research the agency, understand the fees, and compare all available options. In many cases, the best financial decision is the one made slowly and carefully — not emotionally.

Credit counseling may help some people, but for others, it can become an expensive detour that delays true financial recovery.